Insurance Edition: 2026 Privacy Benchmarking Report

- Incident volume declined, but risk remains concentrated. Insurance saw a 6.84% decrease in incidents, reflecting operational maturity.

- Third-party incidents drive the highest risk. External events are nearly 6× more likely to result in a breach than internal ones.

- Notification performance continues to improve. In 2025, 24.2% of notifications were overdue, showing progress for the fourth consecutive year.

- Risk is increasingly tied to digital workflows. Electronic incidents remain the dominant source of exposure.

Jump to Section

Fewer Incidents, Persistent Exposure

Insurance experienced a 6.84% decline in incident volume year over year, in contrast to industries like healthcare, where incident volume continues to rise.

This reflects increasing operational maturity. However, as seen across industries, lower volume does not equate to lower risk.

As incident counts decrease:

- Individual incidents carry greater regulatory and reputational impact.

- There is less tolerance for inconsistency in handling.

- High-impact events play a larger role in overall risk exposure.

Insurance organizations are managing fewer incidents, but operating in an environment where risk is more concentrated and less forgiving (often involving third parties or larger data exposure).

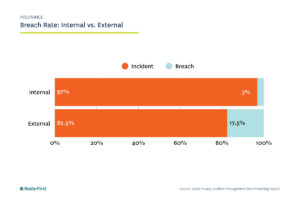

Third-Party Risk is in the Center

Across industries, external incidents remain low-frequency but high-severity, and insurance follows this pattern closely.

- Internal incidents result in breaches at ~3%.

- External incidents rise to ~17.5%, nearly 6× higher.

While external incidents represent a small share of total volume, they are far more likely to escalate into reportable breaches. This mirrors the broader trend where third-party incidents account for a disproportionate share of serious compliance events.

Implication:

Insurance organizations operate within highly interconnected ecosystems. Risk is increasingly driven by partners, vendors, and external data flows, making vendor oversight and consistent cross-organizational response critical.

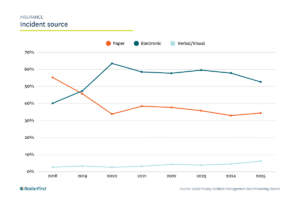

Risk Is Concentrated in Electronic Channels

Incident patterns in insurance are dominated by electronic sources, consistent with broader industry trends where digital channels account for the largest share of incidents.

At the same time:

- Paper incidents remain steady (at around 35%)

- Verbal/visual incidents remain a small portion of overall activity (although growing YoY).

This reflects the industry’s reliance on digital ecosystems, including claims processing platforms, customer systems, and third-party integrations.

Electronic incidents introduce a different risk profile. Compared to paper-based events, they are more likely to:

- Involve larger datasets.

- Spread across systems and partners.

- Escalate more quickly.

Implication:

As in other industries, privacy risk in insurance is becoming more system-driven and scalable, requiring consistent intake, triage, and assessment for digital incidents.

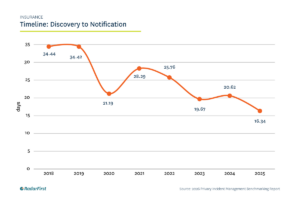

Speed Is Improving, but Execution Gaps Remain

Insurance organizations have made measurable progress in reducing response timelines, aligning with broader industry improvements in operational speed. This allowed insurance companies, for the fourth consecutive year, to shorten the Discovery-to-Notification time.

However, meeting deadlines consistently remains a challenge. 24.2% of notifications are overdue, though improving year over year (this year is the second-best since 2018).

Compared to industries like healthcare, which benefit from longer regulatory timelines, insurance operates under tighter constraints, increasing execution pressure.

Implication:

Improving speed is necessary, but not sufficient. Organizations must focus on consistent execution within regulatory timelines, ensuring that faster responses translate into on-time compliance.

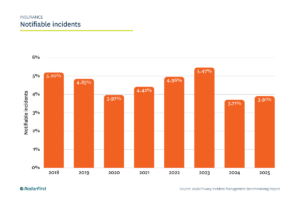

Notifiable Incidents: Lower Rates, Higher Scrutiny

Insurance organizations report a relatively low percentage of incidents requiring notification, with 3.91% of incidents classified as notifiable, below the all-industry average and significantly lower than healthcare.

While this suggests a lower regulatory burden, it also shifts pressure to decision-making. With fewer clear-cut cases, determining what is reportable becomes more nuanced and more likely to be scrutinized.

Implication:

In insurance, risk is increasingly defined by how consistently and defensibly incidents are assessed, making structured decision-making and documentation critical for audit readiness.

Summary

Insurance is operating in a more controlled but still exposed risk environment. While incident volume has declined, risk remains concentrated in external dependencies and electronic systems, where incidents are less frequent but more likely to escalate.

At the same time, improving timelines and overdue rates signal growing operational maturity, but consistent execution under pressure remains critical.

To stay in control and audit-ready, privacy teams need more than process; they need structured, repeatable workflows supported by purpose-built tools like Radar Privacy to ensure consistency, documentation, and defensibility at scale.

Bottom line:

Risk in insurance is shaped by interconnected systems and third-party exposure, requiring coordinated, consistent, and scalable incident management.

Download full report 2026 Privacy Benchmarking Report.

Related Posts

Insights on Privacy, AI Risk, and Compliance

Let’s Get Started

Trusted by leading organizations, RadarFirst enables teams to manage incidents with speed, consistency, and defensibility by standardizing how incidents are captured, assessed, and actioned.