Recent Resource

Featured Resource

Guide

Understanding the NAIC Insurance Data Security Model Law

Provisions, State-by-State Adoptions, and Notifications

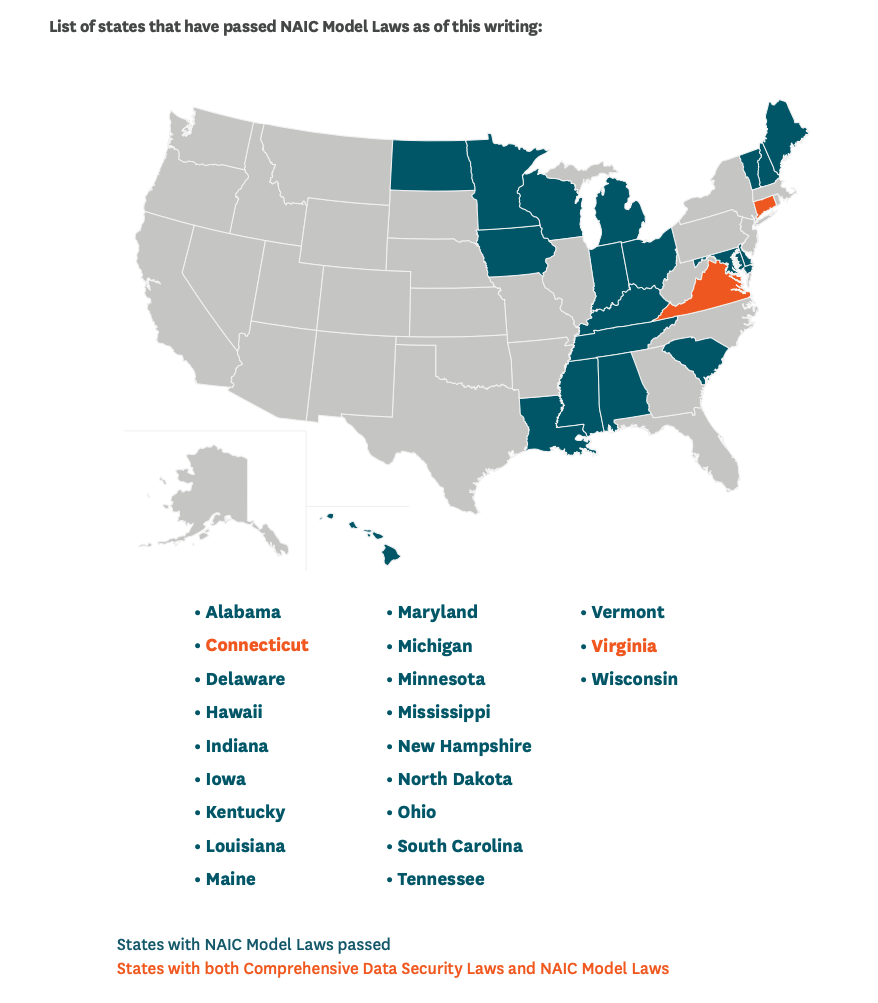

In June 2021, RadarFirst published a blog about the rapid adoption rate of NAIC Model Laws. In the year since, the number of states that have passed data laws based on the NAIC model has more than doubled (rising from 10 states to 21 at the time of this writing).

Table of Contents

- Introduction to the NAIC Model Law

- Urgent Adoption to Forestall Intervention

- Data Management Provisions

- Nuances Vary by State

- Predictions for the Insurance Industry

What is the NAIC?

State governments, not federal agencies, have preeminence over the insurance industry (as defined by the McCarran-Ferguson Act of 1945). Thus, it is up to each state to pass and enforce laws governing insurance companies. Each state has its own chief insurance commissioner to manage this function. To establish a consistent set of standards for state-by-state regulation of the industry, the 50 state insurance commissioners, along with one from the District of Columbia and five from U.S. territories, formed the National Association of Insurance Commissioners (NAIC).

This organization provides regulatory support to the individual states and territories by offering model laws that can be adopted wholesale by a state legislature or modified to accommodate unique state-by-state differences.

The NAIC drafts model laws for states governing many aspects of the insurance industry. When RadarFirst writes about the NAIC Model Law, we refer specifically to the Insurance Data Security Model Law (MDL 668).

Introduction to the NAIC Model Law

The NAIC Model Law (Model Law)—known formally as the Insurance Data Security Model Law—was written by the National Association of Insurance Commissioners (NAIC) to serve as a model for each U.S. state, district, and territory to use in drafting its own legislation governing how the insurance industry will safeguard and manage individual customer data.

The NAIC saw a need for this law as a response to the growing number of large insurers experiencing data breaches. Providing a mechanism for state governing bodies to address consumer needs and concerns was a way to forestall federal intervention in the industry in response to those breaches.

Since 2017, when it was finalized, the Model Law–or a modified\ version thereof–has passed in 21 states.

States That Have Adopted NAIC

NAIC Calls for Urgent Adoption to Forestall Federal Government Intervention

The existence of pre-vetted language specifically designed to govern the insurance industry’s use of data has meant that these NAIC Model Laws tend to move through the state legislatures more quickly than comprehensive cybersecurity laws, which can spend years in back-and-forth revisions and negotiations. As of this writing, only five states have passed comprehensive privacy bills, while 21 have passed data laws specifically related to the insurance industry.

In addition to the relative efficiency of adopting pre-vetted legislation, the pace of adoption of the Model Law has been spurred by a report issued by the U.S. Treasury Department in October 2017. In the report, the U.S. Treasury urged states to adopt the NAIC Model Law within five years. If the Model was not adopted and implemented widely, the report recommended that Congress act by passing legislation setting forth uniform requirements for insurer data security.

As the five-year recommended adoption period winds down, companies can expect to see more states and districts adopt the NAIC Model Law in the second half of 2022.

Understanding Data Incident Management Provisions in the NAIC Model Law

While the NAIC Model Law delves into the details of managing and protecting data, for the purposes of this white paper, we will focus solely on the major provisions related to Data Incident Management and Notification. The Model Law provides several key aspects for incident response, including:

Notification Window

The notification window refers to how long an organization has to notify the State Insurance Commissioner after confirming that an incident occurred. The Model Law as written requires notification, “as promptly as possible but in no event later than 72 hours from a determination that a Cybersecurity Event has occurred.” The law goes on to detail the conditions that define an event based on whether the insurance provider, the impacted consumer(s), or both, are domiciled in the state.

Threshold for Notification

The Model Law requires notification to the office of the State Insurance Commissioner (and other applicable oversight bodies as required by law) as promptly as possible, but in no event later than 72 hours from a determination that a Cybersecurity Event has occurred when either of the following criteria has been met:

- (1) This State is the Licensee’s state of domicile; or

- (2) The Licensee reasonably believes that the Nonpublic Information involved is of 250 or more Consumers residing in this State and that is either of the following:

- (2a) A Cybersecurity Event impacting the Licensee, for which notice is required to be provided to any government body, self-regulatory agency, or any other supervisory body pursuant to any state or federal law; or

- (2b) A Cybersecurity Event that has a reasonable likelihood of materially harming: (i) Any Consumer residing in this State; or (ii) Any material part of the regular operation(s) of the Licensee.

Notification Content

The Model Law details 13 separate categories of information that must be considered in the notification to the Commissioner.

Data Breach Incident Information Required by NAIC Model Law

- Date of the event

- Description of how information was exposed, including the roles of third-party service providers

- How the cybersecurity event was discovered

- Whether any lost, stolen, or breached information has been recovered, and if so, how

- Identity of the source of the cybersecurity event

- Whether Licensee has filed a police report or notified regulatory, government, or law enforcement agencies, and, if so, when

- Description of the specific types of information acquired without authorization

- The period during which the cybersecurity event compromised the information system

- The total number of consumers in the state affected by the event

- Results of internal review identifying a lapse in automated controls or internal procedures, or confirming that all computerized controls or internal procedures were followed

- Description of efforts being undertaken to remediate the situation that permitted the vent to occur

- Copy of the licensee’s privacy policy and a statement outlining the steps the licensee will take to investigate and notify consumers affected by the cybersecurity event

- Name of a contact person who is familiar with the event and authorized to act for the licensee

All data breach incident information required by the NAIC Model Law (and more) is tracked in the Radar® Privacy incident management platform to help businesses comply with notification requirements on a state-by-state basis.

Who Must Be Notified

The Model Law requires notification to be sent to the State Insurance Commissioner, as well as to any other governing bodies specified in other state legislation on the books. The Model Law leaves the determination of whether to notify individual consumers to the state’s discretion, with some states including a specific requirement to notify consumers, while others leave the requirement under the state’s data breach notification law.

Other incident response topics the Model Law addresses include:

- How to handle incidents impacting third-party service providers

- How to handle incidents impacting reinsurers

Click here to read the NAIC Model Law in full.

Nuances in Data Incident Management Requirements Vary by State

In theory, the NAIC Model Law provides a standardized approach to governing how companies must manage and respond to data breaches and other incidents. In practice, we have observed that state-by-state enacted laws exhibit notable variances from the Model, reflecting the distinct preferences and business climates of individual states.

When it comes to incident management and response, the nuances that are particularly important to note within the laws include: differences in the notification window, differences in the threshold for notification, the types of consumer information that – if breached – would be considered a data incident, the individuals and oversight bodies that must be notified, and as mentioned above, whether and in what circumstances consumers must be notified.

Data points such as state, effective date, and notification window are only three of 18 categories of compliance the Radar® Privacy automated platform tracks and uses to determine incident risk.

Unlike other state laws, Vermont’s H.515 does not impose notification obligations on licensees following a cybersecurity event. Instead, licensees are bound by the notification requirements of the Vermont Security Breach Notice Act, 9 V.S.A. § 2435.

Additionally, some adoptions of Model Laws specify a different notification threshold for domiciled and non-domiciled insurers or if notice is required to another regulatory body, adding more challenges for insurers or producers who operate in multiple jurisdictions in designing their compliance programs to accommodate varying obligations.

Notification Windows Range from 72 Hours to 10 Days

A detailed review of state-adopted versions of the NAIC Model Law shows that the notification window for a cybersecurity event ranges from 72 hours (the Model guideline), to three “business days,” to 10 business days in some cases.

In states where other consumer data breach notification laws are in place, of course, responding to an incident is further complicated by the fact that those additional laws may specify a completely different set of notification windows.

The likelihood that many states will pass their own comprehensive cybersecurity laws in the next few years will undoubtedly add further complexity. Without an automated response system, companies will struggle to meet deadlines and avoid penalties.

Differing Definitions of Nonpublic (Consumer) Information

The Model Law sets forth the definition of information that would be considered nonpublic as follows:

- Business-related information that, if released, would cause material harm to the licensee.

- Consumer data in which a name, number, or other personal mark or identifier is combined with any of the following: Social Security number, driver’s license or ID number, account numbers, or security codes or passwords.

- Health and mental health data, or treatment data, or payment data relating to health or mental health data of the individual or a family member.

While most states have adhered to these definitions when adopting the NAIC Model Law, a few notable exceptions include states that do not include business-related information and a state that has added military IDs and passport numbers to its list of nonpublic consumer data.

These existing exceptions suggest that other states will continue to adapt the definition as they pass their own NAIC Model Laws. An automated risk assessment tool will be instrumental in understanding which data is implicated in each jurisdiction.

Widely Varying Requirements Regarding Whom to Notify

As mentioned above, the NAIC Model Law requires notification of an incident to be made to the State Insurance Commission and to any other governing bodies named in any other relevant legislation. Furthermore, the question of whether to notify consumers is left to the states, depending on whether other cybersecurity laws are in place.

Because nearly every state has a different set of laws governing individual industries, data formats, and incident types, it is a foregone conclusion that states with adapted NAIC Model Laws will have different notification and reporting obligations. A response platform that tracks required notifications, along with a module to customize notifications according to state requirements, will save days, if not weeks, of work.

Compliance Grace Periods Add Further Nuance

The NAIC Model Law suggests that companies have up to a year following the law’s enactment to develop and implement an information security program (which must be delivered to the State Insurance Commission). Additionally, the Model Law allows for an extra year to develop a program for managing data used or stored by third-party providers. States are likely to determine their own compliance timelines, but even if they do not, the Model timeline is already complex.

Taken in full, the nuances inherent in complying with NAIC Model Laws, state by state, drive the pressure on privacy teams higher and higher.

Predictions for Data Incident

Management Response and the Insurance Industry Moving Forward

With only a few months until the federal government’s recommended adoption and implementation period ends, Radar® Privacy anticipates that many states will enact NAIC Model Laws in the second half of 2022.

However, privacy teams should not consider any new legislation to be a one-and-done set of guidelines. The NAIC is currently reviewing and updating the NAIC Model Law discussed in this white paper (MDL 668), as well as Model Law 672 Privacy of Consumer Financial and Health Information Regulation.

Organizations should expect that when NAIC issues the new language for these laws, states will respond with amendments to their already adopted NAIC Model Laws, resulting in a constantly shifting set of requirements for incident management and response.

Privacy teams that rely on manual, one-size-fits-all incident response processes or have previously found success tracking new laws manually will need to transition to automated risk assessment and intelligent incident management software platforms to keep up with the nuances and complexities required on a state-by-state basis.

Companies that demonstrate a commitment to creating a culture of responsible and responsive data management– including a strong infrastructure of digital tools to automate their processes for on-time, complete incident responses – will likely fare better when facing the inevitable data breach.

Enforcement Measures Will Focus on Compliance, Consumer Awareness

In most states, insurance companies have a period of eight months to a year between the law’s passage and its effective date to develop their data plan, so we will likely begin to see enforcement measures in states that are one year or more past the effective date.

State enforcement of NAIC Model Law provisions may resemble enforcement practices for other insurance industry noncompliance.

In general, the NAIC describes enforcement as a process of investigations, recommendations to bring the company into compliance, and if called for, a combination of civil penalties, license suspension, or license revocation.

For example, a data breach incident in Texas affected the state’s own office for workers’ compensation insurance. The state agency’s response included:

- Working with a forensic company to investigate the nature and scope of the event

- Reviewing and enhancing policies, procedures, and security efforts

- Offering 12 months of credit monitoring and identity protection services at no cost to those who may have been affected

- Providing a dedicated helpline for questions about the event

State Insurance Commissioners have yet to establish precedents for the types of civil penalties that might be levied, but state laws outline penalties ranging from $100 to $150,000 or more if companies fail to address known weaknesses in their data management plans. Most states do not allow consumers a private right of action, but a few exceptions exist, specifying actual damages only.

Companies Will Use Data Incident Benchmarking as Decision Intelligence

As companies automate their data incident management and response, they will be able to leverage data breaches to their advantage, enabling their privacy teams to make informed decisions and differentiate their companies from competitors in the industry.

The Radar Privacy Guide to Digital Transformation for Privacy Incident Management argues that to reap the benefits of digital transformation, your organization must possess decision intelligence. According to Gartner, which coined the term, decision intelligence is the integration of data, analytics, and automation to create platforms that support, augment, and automate decisions. In other words, decision intelligence is the ongoing, automated, and analyzed data you need to make strategic business decisions.

Decision intelligence allows your organization to:

- Evaluate historic decisions and processes for improvements

- Create employee awareness training to change practices and processes

- Run models to drive future decisions

- Identify response processes across the organization that could be simplified or, better yet, automated.

The Radar Privacy Intelligent Incident Management Platform enables you to automate your data processes, collaborate and communicate across teams, and benchmark your incident management and response activities, generating an ongoing source of decision intelligence for your organization.

Approach to Data Incident Management and Response Will Become an Intangible Asset in the Valuation of a Company

As companies begin to differentiate themselves based on their approach to data management and incident response practices, cybersecurity competencies will become a valued component of brand identity. More states are likely to follow Texas’s lead in maintaining a public list of companies that have experienced data breach incidents, as well as how the companies responded.

Customers will make purchasing decisions based on the strength and responsiveness of a company’s data incident response, and analysts and investors will assign a monetary value to a company’s commitment to digital transformation of data management and incident response. A company’s position in mergers and acquisitions will be directly impacted by its cybersecurity profile.

Digital Transformation of Data Incident Management and Response Will Be Critical to Meeting Complex Requirements

The complex legal framework governing data management in general, and data within the insurance industry specifically, has grown to the extent that manual tracking and response will be nearly impossible in the very near future (if not already).

Privacy leaders and teams require robust, third-party software platforms to avoid over- or under-notifying governing agencies and consumers, and to prevent incurring civil penalties, or worse, suspension or revocation of a license to act as an insurance provider.

The Radar Privacy Intelligent Incident Management Platform offers flexible and reliable capabilities to support compliance with new state adoptions of the NAIC Insurance Data Security Model Law. In real-time, Radar® Privacy:

- Determines if the incident qualifies as a notifiable cybersecurity event

- Provides a jurisdiction-by-jurisdiction risk of harm analysis

- Alerts you to notification timelines for each jurisdiction

- Enables quick outreach with notification templates

- Publishes state-specific law overviews to support your understanding of a law’s complexity

We track new laws and amendments to existing laws, keeping our automated platform up to date. This ensures your business can maintain best practices in data incident management and response with confidence. As a result, consumer and market confidence in your brand will grow. The need to transform your data practices and utilize the latest technology solutions has never been more vital for your business.